I know not everyone wants this; some might even hope to work beyond the age of 60, due to various reasons like financial commitments, children, or are simply unsure of what they can do with the free time. However, the situation is not the same for people who know what they want to do, but do not have the time to do it now, as they need to spend their time working in exchange for money to settle whatever financial commitment that they have, and continue to hope that they will have enough money as soon as possible in order to stop working and start doing what they like.

The main obstacle that we can see here is money.

So, how can we resolve this issue? It is quite impossible to live debt free in Malaysia especially if you own a house. The average instalment tenure for a housing loan is 30 years nowadays. Imagine a person buying a house at the age of 35; he or she will have to service the loan even after retirement age! No wonder there are so many people who hope that their retirement will never come as they still have huge financial burden even up to the age of 60!

If we sit back and reverse the time to 20 or 30 years ago, we would realize that the generation before is able to fund their house with a bank loan of 10 to 15 years, which is to say that our earning capacity has been reduced by half (approximately) compared to the earlier generation!

Another problem that will arise if a person has a 30 years housing instalment is that the money that they can save for their retirement will be greatly reduce compared to earlier generation. This is due to the fact that the earlier generation will still have 15 years’ worth of employment time for retirement savings after they have fully settled their 15 years housing instalments. The same cannot be said of the current generation.

So, for the current generation, how do we retire early?

Please be reminded that the following suggestions are only suitable for those who do not own a house yet and is still currently staying with their family. If you want to buy a house and retire early, you can either:

1) Chose to buy a cheaper house, a house that you can afford to settle the loan in 10-15 years’ time.

2) Postpone your plan to buy a house. Save as much as you can in the first 10-15 years of your career and invest your savings wisely for optimum growth. Only look for your house options after you have saved sufficiently.

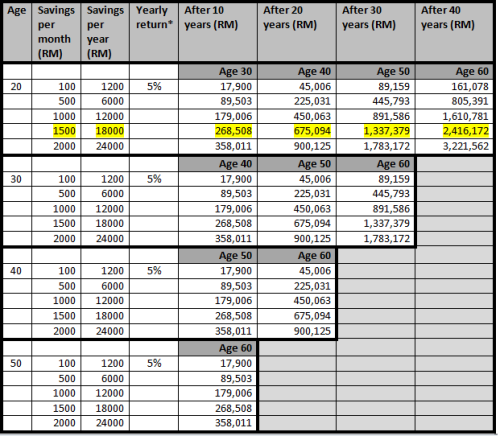

Remember the power of time compounding factor? The money that you saved during your younger age is definitely more valuable than the money you save when you are approaching retirement age due to the compounding interest effect. Below is a table that illustrates this:

Table 2: Total savings worth in future by starting age and by savings per month

*Assumption: Average return from your total portfolio.

The table above illustrates the estimated total savings that you can get in the future by referring to the age that you start your savings and how much savings you have per month. For example, if you start at the age of 20, and are able to invest RM1,500 every month or RM18,000 every year with a rate of 5% return per annum, you will get RM268,508 after 10 years or RM675,094 after 20 years, as per highlighted in yellow above.

The table is only used as reference and is a rough estimate. It assumes a person has zero savings before this. Of course, it will be much easier and faster if the person already has some savings even since childhood, or if they have bigger capability and discipline to save more money when they are going up the career ladder. All this leads to a shorter time frame in achieving their financial goals.

Different people have different goals. It will be much easier to achieve your goal if it is much simpler. For example, let say I want to have around RM3500 per month. If you refer to table 3 below, you will notice that if I start saving by age 20, investing RM24,000 every year with a return of 5% per annum, after 20 years’ time when I reach the age of 40, I will have earned interest per month of RM3,751 for my perusal. It is the time when you have savings of RM900k when you refer to table 2 above.

Table 3: Total interest available per month for usage by starting age and by savings per month

*Assumption: Average return from your total portfolio.

The target that I have set just now is for RM900k savings (start saving at age of 20, retire by age of 40). If I postponed my plan to buy a house, and invest the portion of money that I initially planned to use for the house instalment, I would have reached the RM900k target well before the age of 40, right? And if the RM3,500 interest per month is sufficient to cover the instalment for a cheaper house, I will gladly retire before age 40 and start living a simple life. It will also be easier for couples to achieve their target with the combined savings of two people.

Of course, what I have illustrated above may not be practical and suitable for everyone. Those who have bigger vision and dream, those who have opportunity to invest their money in properties or businesses to earn much more profit, those who loves their work life, etc., should continue to work.

Everything involves risks, and it is about personal choice. The method above is only suitable for people who wants to retire as early as possible and enjoys a simple life. Hope you enjoy this article. Thank you.